By The Young Wizard - 25 Oct 2020 16:09

- 25 Oct 2020 16:09

#15130120

Hello,

I think that the empirical evidence - so far as I can judge - that the rate of profit in capitalism does have a historical tendency to fall. However, I still seem to be intellectually unconvinced that at the bottom of that is the law of value (or labour theory of the value of commodities or whatever).

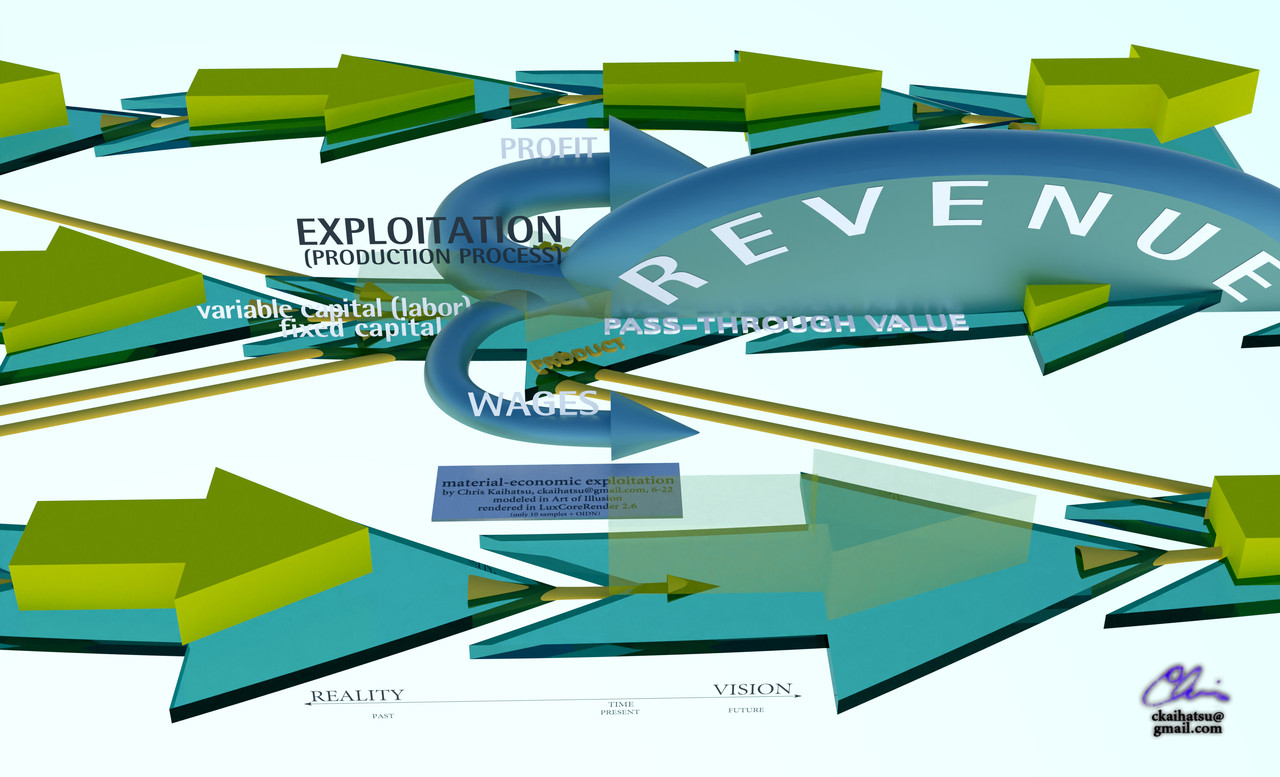

The most impressive book I've read about this is Reclaiming Marx's Capital by Andrew Kliman. Roughly, he argues for an interpretation where a capitalist system only ever produces a certain volume of value at a given time, which due to the tendency of the rate of profit to fall, will tend to decrease (though not smoothly or without interruptions). Prices can deviate value - and so presumably the total mass of prices from the mass of value - but (and this is just my assumption, having not got through all my Marx) if prices rise much in excess of value, then we are just creating ficticious capital. I think Marx's theory really needs this tethering of prices to value - if we don't have that, then maybe we still can get the law of the tendency of profit to fall operating, but there will be even more additional factors at play, so it may win out less.

Anyway, I was wondering about what it would mean today if price was tethered to value in this way. Value and price are both social facts - they don't exist outside human society. So what kind of behaviour does following something like value theory require. I was thinking that it could be something like when you are a producing goods for sale, you pay attention to how much time you put into them. If they take too long to produce - in comparison to the goods you require from others, then you will try to demand something more equivalent. You and the other producers will see your goods as having higher value in comparison. If some process comes along to make your good more efficiently, then people will go with that, and you will have to adapt or be progressively at a loss. Hence the average social labour time is important, as Marx thought. But I still don't feel I've thought through hardly anything here. Obviously this will only work for prices for items where nothing else intervenes. Acquire a rare work of art, within the right kind of legal and social system, and you will be able to extract alot of currency without having to think (too much) about how much time you will put into it.

Finally, I was also thinking about how preference functions fit into all this. I've heard some Marxists be very dismissive of the whole idea - but from when I used to be at uni, I remember working out that I didn't so much think that the idea of people's aims and desires being organised into preference functions as outlandish, but more just that it's a much more formal idea that it is usually presented. The important thing to remember about all such models is to ask whether they import anything in to themselves about the ultimate aims or concerns of the agents involved. If they don't, then they really aren't saying anything about human nature - just possible ways people could think through how to meet their aims. And how you meet your aims can be part of the aim, so we can neither conclude that people should arrange their desires into preference rankings, or indeed do. If this is the case, the model at the "heart" of neoclassical economics isn't incompatible with Marx, as that model doesn't even say what those economists think it does. It can be perfectly well re-expressed what Marx says about the formation of value in preference function language - whether it makes sense to is another matter - as that language is just a way of expressing attitudes of beings who are able to compare their aims and decide which are more or less important in a way that has a formal elegance that some theorists desire.

What do people think of this? What are the objections?

I think that the empirical evidence - so far as I can judge - that the rate of profit in capitalism does have a historical tendency to fall. However, I still seem to be intellectually unconvinced that at the bottom of that is the law of value (or labour theory of the value of commodities or whatever).

The most impressive book I've read about this is Reclaiming Marx's Capital by Andrew Kliman. Roughly, he argues for an interpretation where a capitalist system only ever produces a certain volume of value at a given time, which due to the tendency of the rate of profit to fall, will tend to decrease (though not smoothly or without interruptions). Prices can deviate value - and so presumably the total mass of prices from the mass of value - but (and this is just my assumption, having not got through all my Marx) if prices rise much in excess of value, then we are just creating ficticious capital. I think Marx's theory really needs this tethering of prices to value - if we don't have that, then maybe we still can get the law of the tendency of profit to fall operating, but there will be even more additional factors at play, so it may win out less.

Anyway, I was wondering about what it would mean today if price was tethered to value in this way. Value and price are both social facts - they don't exist outside human society. So what kind of behaviour does following something like value theory require. I was thinking that it could be something like when you are a producing goods for sale, you pay attention to how much time you put into them. If they take too long to produce - in comparison to the goods you require from others, then you will try to demand something more equivalent. You and the other producers will see your goods as having higher value in comparison. If some process comes along to make your good more efficiently, then people will go with that, and you will have to adapt or be progressively at a loss. Hence the average social labour time is important, as Marx thought. But I still don't feel I've thought through hardly anything here. Obviously this will only work for prices for items where nothing else intervenes. Acquire a rare work of art, within the right kind of legal and social system, and you will be able to extract alot of currency without having to think (too much) about how much time you will put into it.

Finally, I was also thinking about how preference functions fit into all this. I've heard some Marxists be very dismissive of the whole idea - but from when I used to be at uni, I remember working out that I didn't so much think that the idea of people's aims and desires being organised into preference functions as outlandish, but more just that it's a much more formal idea that it is usually presented. The important thing to remember about all such models is to ask whether they import anything in to themselves about the ultimate aims or concerns of the agents involved. If they don't, then they really aren't saying anything about human nature - just possible ways people could think through how to meet their aims. And how you meet your aims can be part of the aim, so we can neither conclude that people should arrange their desires into preference rankings, or indeed do. If this is the case, the model at the "heart" of neoclassical economics isn't incompatible with Marx, as that model doesn't even say what those economists think it does. It can be perfectly well re-expressed what Marx says about the formation of value in preference function language - whether it makes sense to is another matter - as that language is just a way of expressing attitudes of beings who are able to compare their aims and decide which are more or less important in a way that has a formal elegance that some theorists desire.

What do people think of this? What are the objections?

")

- By Sherlock Holmes

- By Sherlock Holmes - By wat0n

- By wat0n - By Tainari88

- By Tainari88